EN

Home > Guide to Life Insurance in Hong Kong

Guide to Life Insurance in Hong Kong

What is life insurance? Which type is right for you? And how much coverage do you need?

Last update:

5th November 2025

5th November 2025

What is life insurance? Which type is right for you? And how much coverage do you need?

Last update: 5th November 2025

Life is unpredictable. We can’t always plan ahead for every challenge in life, but it’s never too late to start preparing.

Purchasing life insurance is an important decision, especially when you think of it as a commitment for the next 10 or 20 years, or even more. When looking for a policy, you may find yourself swimming in a sea of jargon and questions: What’s the difference between a term life policy and a whole life policy? How does life insurance work? How much does it cost? Which one is right for me? Look no further. Alea is here to answer all your questions about life insurance.

What is life insurance?

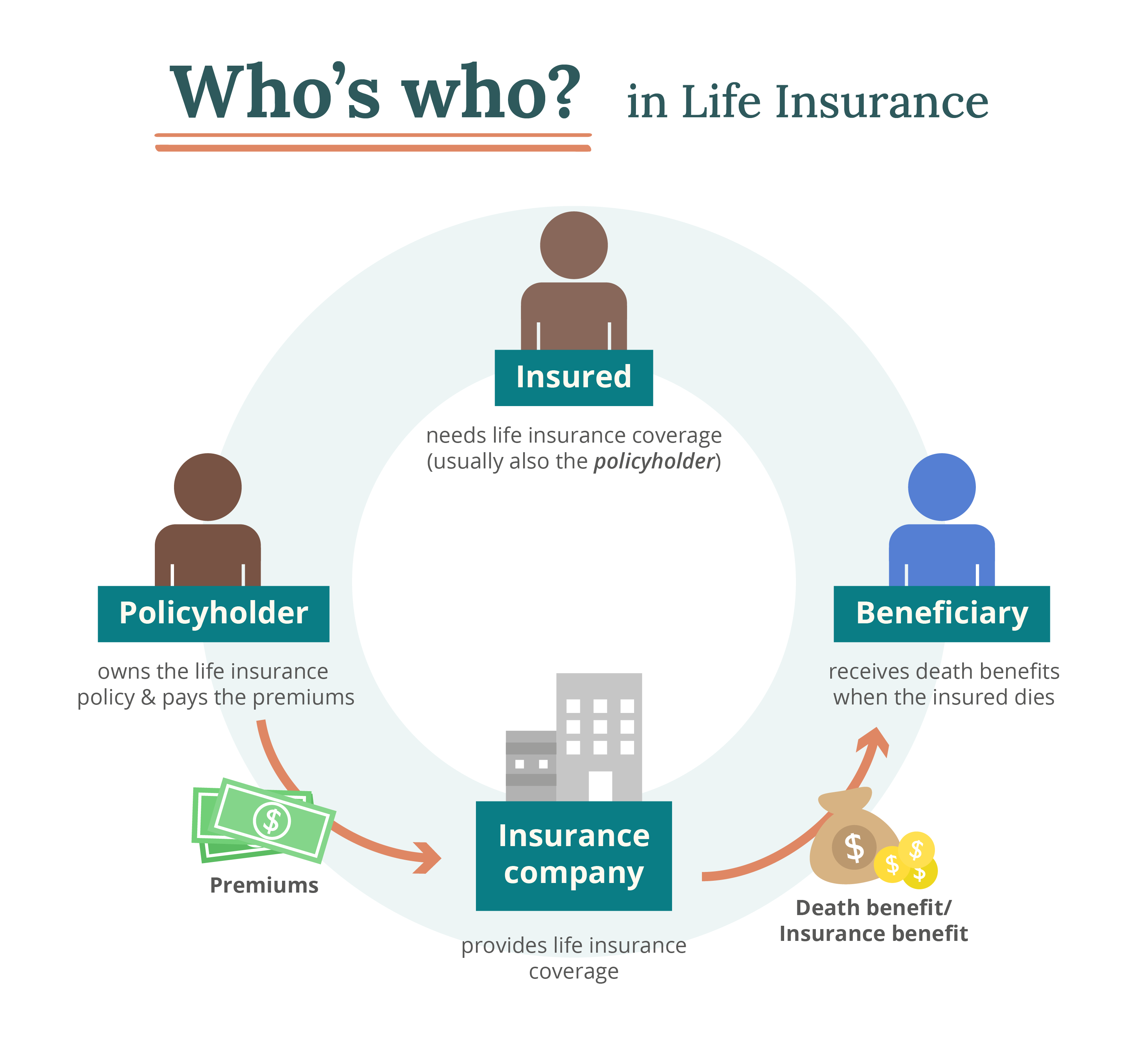

Life insurance is a risk management tool that aims to provide financial security for your family members or any named beneficiary upon the unfortunate event that you (the insured person) pass away; or with critical illness insurance, for (your) diagnosis and treatment costs as well.

Over time, insurance providers have developed an array of life insurance products with different levels of cover, benefit terms, financial goals, etc. For example, some life insurance products contain a saving or investment component and have gained popularity as long-term wealth management tools.

How does life insurance work?

Whichever life insurance plan you opt for, over the policy term, you as the policyholder have to pay a monthly or annual premium in exchange for a lump sum known as the death benefit paid to your beneficiary/beneficiaries when you/the insured person dies; whereas critical illness plans comprise a lump sum benefit upon diagnosis of a critical condition.

In Hong Kong, all insurance benefits are tax-free, meaning that the beneficiary can receive coverage in full without deducting the tax.

Oftentimes the policyholder may also be the insured, but one can also take out life insurance on a spouse, a parent, a child or even a business partner with their consent, at the same time be their beneficiary.

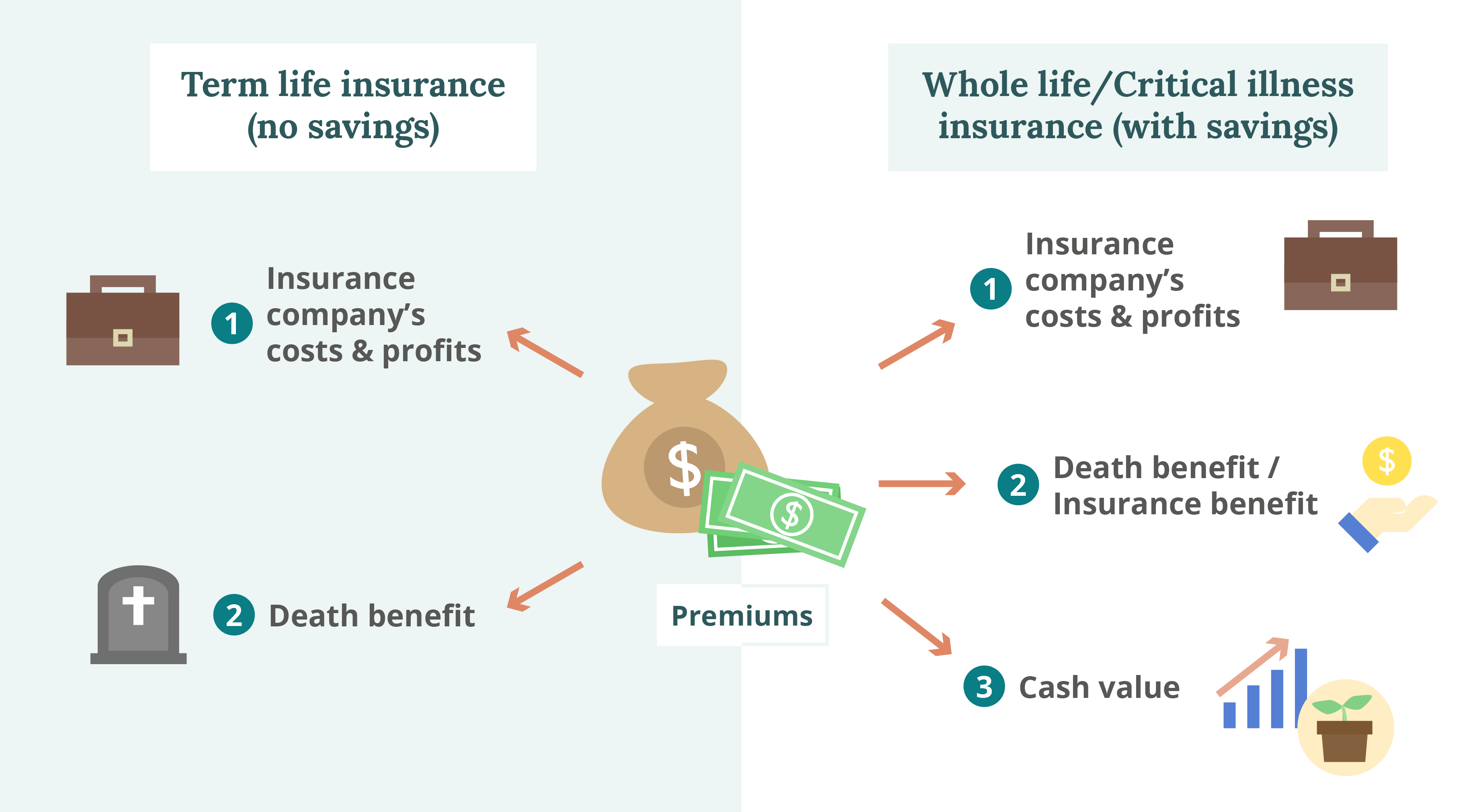

Cash value

Cash value is a portion of the premium that earns interest in a life insurance plan and can be withdrawn by the policyholder.

Take a whole life policy or a critical illness policy as an example. The premium paid will go to the insurance benefit, the insurance company’s costs and profits, and the remaining part to the cash values, earned via the insurance company’s investments. Contrarily, a term plan normally has no cash value.

Cooling-off period

In Hong Kong, the Insurance Authority requires insurance companies to provide a 21-day cooling-off period upon delivery of the life insurance policy or the Cooling-off Notice to protect the interests of the policyholder. During this period, you can reflect on your decision and cancel the policy for a full refund. The insurer bears the responsibility to clearly explain this right to clients.

Types of life insurance

Life insurance can be categorized into three main types: critical illness insurance, term life insurance and whole life insurance. They serve different purposes and have different costs and conditions.

Whole life insurance

Whole life policies offer lifelong protection, or sometimes protection until 100 years old. They often come with a savings element and a fixed premium that must be paid within an optional installment period (e.g. 5 years to 25 years). Unlike term policies, premiums of whole life policies stay the same regardless of your age. Owing to its ability to accumulate cash value and its prolonged coverage, whole life insurance typically has much pricier premiums that can be four or more times that of term life insurance.

Learn more: Guide to whole life insurance in Hong Kong

Term life insurance

Term life insurance covers the death of the insured only for the premium-paying term, which is usually set at 10, 20 or 30 years. Most term life policies only cover up to a certain age, e.g. 65 years old. As the policy term ends, the policyholder has the option to extend their policy or convert it to a whole life policy (which would require an underwriting). You can expect premiums to increase exponentially at each renewal as you get older.

If you decide to discontinue your coverage after the term ends, the plan simply expires with no retrievable value. An exception is Return of Premium (ROP) plans, a subcategory of term life insurance that gives you the option to refund the total amount of premiums paid when you outlive the policy, but these are attached with higher premiums than regular term policies.

Term life insurance in general does not have a savings component and is more suitable for those who are exposed to substantial financial risks, such as mortgage, loans, and debt.

Learn more: Guide to term life insurance in Hong Kong

Critical illness insurance

Hong Kong has the world’s second most expensive private healthcare system. While your health insurance may be able to get you covered for most common conditions, in the face of a life-threatening condition like cancer, organ failure or stroke, treatment and hospitalization can cost millions and easily exceed your health insurance’s coverage. What’s more, when diagnosed with severe illness, many are unable to work or earn income for a period of time. This is where critical illness insurance kicks in.

Critical illness insurance secures you financially with a lump sum payment upon diagnosis of a serious health condition. Such coverage safeguards your family’s quality of living by providing financial support for daily living expenses, rents, mortgage payments and so on.

Every insurance company has different definitions for “critical illnesses,” but generally most of these policies cover 60-70 named illnesses or conditions. Note that any pre-existing conditions may lead to exclusions or premium loadings.

Note: A waiting period of 1-3 years may apply for reimbursements for the same conditions

Learn more: Guide to critical illness insurance in Hong Kong

Quick compare: Whole life, term life and critical illness insurance

| Whole life insurance | Term life insurance | Critical illness insurance | |

|---|---|---|---|

| Period of coverage | Lifetime | Within the term of 10/20/30 years | Lifetime |

| Insurance benefit | Death benefit paid to beneficiaries | Death benefit paid to beneficiaries | Lump-sum benefit paid to the insured upon diagnosis of a critical illness |

| Premiums | - Higher - Level premium paid within an installment period of 5-25 years | - Lower - Level premium, which may increase with age at end of term / policy conversion *30 years plan with Return of Premium (ROP) option | - Highest - Level premium, paid within an installment period of 5-25 years |

| Savings element | Yes, with additional cash values/dividends | No | Yes, with additional cash values/dividends |

| Suitable for | Those who want lifelong coverage or a savings component | Those with liabilities, i.e. loans, mortgage, debts to repay | Those who want lifelong coverage for critical illness treatment or a savings component |

Group life insurance

Some large companies would also offer group life insurance to their employees, particularly for senior management staff. Most employers favor term life policies that are renewable yearly. Such plans generally have no savings element and will terminate if you switch or quit your job. Therefore, it is important to get your own insurance, independent of your employment status.

Do I need life insurance?

Whether you need to be insured or not all comes down to your life planning. Do you have a family to support? Liabilities to repay? Plans for retirement? The list goes on.

The most common reason to get life insurance is to protect your children or loved ones against uncertainties. Some insurers offer specific life insurance plans to cater to specific financial needs through different life episodes, such as:

- Debts

- Mortgage or rent

- Car loan

- Funeral cost

- Education fund

- Living expenses of dependents

- Retirement planning

Different stages of life bring different needs and goals. We never know what the future holds. While it is never too late to take action and get valuable protection, it is recommended to get insured when you are still young and healthy. That way you can lock in a lower premium, have some peace of mind and protect your loved ones in case any health condition arises, which could make you uninsurable in the future.

What is the best life insurance product for me?

Because everybody has unique needs, there is no one-size-fits-all solution to life insurance. That said, we’ve put together some comparison guides to give you an idea of the life insurance products that are available in Hong Kong.

Comparison guides:

- Best term life insurance plans

- Best whole life insurance plans

- Best critical illness insurance plans

Consider a “split” approach

At Alea, we have seen growing interest in critical illness products in Hong Kong in recent years. It is also common for people to split their investments into a critical illness policy, for their own use in case of a terminal condition, plus a whole life policy, to leave peace of mind to their family if the unfortunate happens.

How much life insurance coverage do I need?

Life insurance products come in all shapes and sizes. Most insurers set a minimum life insurance coverage at US$ 30,000-50,000, whereas there is generally no maximum, but more requirements may apply when the amount goes beyond US$ 500,000.

You can try the Life Protection Coverage Calculator by the Investor and Financial Education Council to estimate your ideal life insurance coverage. The best thing to do is to talk to your advisor for a more thorough analysis of your needs.

Below are some ideas for how much coverage you might want to have, depending on your circumstance.

Critical illness insurance

At least 1-3 times your annual salary. This covers treatment costs and sustains your family’s living expenses if you must take time away from work because of illness.

Term life and whole life insurance

10-15 times your annual income. This covers your family’s expenses in your absence until your children become financially independent.

Term life insurance

The same amount as your liability (mortgage or loans). This will lift the economic burden from your family.

Factors to consider when buying life insurance

Here are some key factors you may want to pay attention to when choosing a life insurance product for yourself or your family.

Living expenses of dependents

Taking out a life insurance policy helps ensure your family’s quality of living should anything happen to you – especially if your family depends heavily on your income. Take into account how much your family needs when it comes to everyday living expenses and carrying on with their lives in comfort.

Take the amount spent on living expenses (including groceries, entertainment, rent and clothing) and multiply this figure by the number of dependents and the number of years they will need financial support (for instance, until your children become adults). From this figure, subtract your existing savings, investments, MPF and other assets.

Education fund

Raising children is a long-term commitment, and you will want to give them all the best things in life. Childcare, daily living expenses, medical costs, extra-curricular activities and college tuition are a heavy financial burden for many families. A UGC-funded university degree program in Hong Kong costs HK$ 42,100 per year; this number can shoot up to 5-10 times that if you plan to send your kids abroad for studies.

Funeral expenses

Making after-death arrangements in advance can be a great relief for your family. Part of the death benefit can be used towards funeral preparation. Burial, cremation, parting ritual, crematorium or cemetery costs in Hong Kong can range from HK$ 10,000-100,000; the cost depends on the styles and scales chosen. Holding such rituals overseas can be significantly more expensive.

Liabilities to repay

When buying life insurance, consider any outstanding liabilities when determining your coverage. Make sure your mortgages, debts, and loans can be settled even if you are no longer there to support the family.

Inflation

Bear in mind the possible impacts of inflation when you draft the blueprint of your future. In the last decade (2011-2020), Hong Kong saw an average 3% increase per year in the Consumer Price Index (CPI), a widely adopted indicator of inflation. In other words, consumer products today on average cost about 30% more than those 10 years ago.

It is always better to brace yourself with an extra amount for future inflation when calculating costs of living, education, accommodation, medical services and so forth.

How Alea can help you save on insurance

Looking for life insurance?

Alea brings you choice, unbiased advice and personalized service. Get free life insurance quotes today to learn more.

An advisor will be in touch to answer all your questions!

This article was independently written by Alea and is not sponsored. It is informative only and not intended to be a substitute for professional advice and should never be relied upon for specific advice.